FOREWORD

It is my honour and privilege to introduce Thomson Reuters’ 2021 Australia: State of the Legal Market report. This report has been informing law firms and legal departments for seven years. Over that period the legal sector has experienced enormous change and evolution, in particular during the past year. The legal sector that we see today is vastly different to what it was a decade ago. Fuelled by technology, necessity and crisis, the Australian legal industry today is a beacon of innovation.

Last year’s State of the Legal Market revealed that Australian firms were experiencing a spike in demand for legal services. One year on that growth has slowed somewhat, but in the face of softening demand firms are adapting their services to tap into nascent client needs in areas such as regulation and mergers & acquisitions where demand has grown 14.8% and 9.4% respectively.

Law firms are responding to market conditions with strategic approaches and reimagining client experiences. Firms are taking the opportunity to serve clients better, which is helping to strengthen their relationships. The appetite for digital transformation also remains strong. With unprecedented pressure to provide legal guidance flexibly, technology uptake and usage among firms has never been greater.

I’d like to thank our contributors, Eric Chin (Alpha Creates) and Joel Barolsky (Barolsky Advisors) for their dedicated contributions to the report, as well as the broader team of experts at Thomson Reuters and the Thomson Reuters Institute who have yet again delivered the financial intelligence, insight and rigorous research that our customers have come to expect.

INTRODUCTION

At the inception of the American space program in the late 1950s and early ‘60s, the astronauts-intraining needed a way to train for the microgravity environment of outer space before they actually launched on a mission. Everyone who has ever ridden a roller coaster, or even crested a hill too quickly in an automobile has experienced this “zero G” phenomenon, but neither of those options are safe or prolonged enough for training purposes. So, the astronauts began to use a specialised aircraft that would fly up to around 40,000 feet, then go into a steep dive, putting the occupants into what essentially was a controlled free fall but giving them the feeling of weightlessness. It was a tremendous rollercoaster in the sky.

That analogy is an apt illustration of how expectations have shifted over the past year across legal markets in Australia. While the market has presented rapid ups and downs as well as periods of relative calm, much like the astronauts’ rollercoaster in the sky, it has been a stomach-turning ride for many.

The first quarter of the recently concluded financial year started with major concerns about the impact of the global pandemic and the ensuing economic crisis that followed. Many Australian law firms may have wondered if this might be a repeat of the Global Financial Crisis, and some firms enacted various strategies to contain costs, buckle down, and prepare for the worst.

Then, the worst didn’t happen.

In FY 2021, the average firm recorded 2.2% growth in total average law firm hours, a 3.6% increase in average fees worked, and a 3.5% reduction in expenses. In combination, firm profits grew to record highs, with average profit as a percent of revenue growing to 36.8%.¹

Demand² growth in FY 2021 was clearly different from previous years, which saw demand mainly fueled by major events like the Hayne Royal Commission into the banking sector. Across the country, all major cities recorded demand growth with Perth being the standout at 7.6% growth.

After an initial slowdown in the hiring pace early in the year, Australian law firms began to hire again, with the average law firm growing its total number of qualified fee earners³ by 3.4%.

As a possible consequence of the down-swings anticipated during the pandemic, FY 2021 also saw firms investing to a lesser degree in new technology, trying to make the most of existing applications as part of a broader push to rein in expenses. This meant that lawyers and support staff could remain productive as firms implemented work-from-home or hybrid models, but the potential impact on future innovation in the delivery of legal services is, as yet, unknown.

On the whole, the sudden shift to remote working can be considered a success for the Australian legal market, enabling firms to uncover previously unknown efficiencies and providing legal talent within the firm the flexibility and balance they had craved. At the same time, however, lower value work which had previously been completed by other fee-earning professionals may have shifted upward to lawyers, leading them to bill hours at a higher rate that might otherwise had been done by colleagues with less seniority for a lower rate.

Along with the ups and downs caused by the pandemic, the conclusion of the Hayne Royal Commission will signal the end of legal advisory opportunities for which firms had so vigorously competed during the past few years. This will likely produce yet another potential trough for our rollercoaster market, forcing firms to compete in a maturing legal market where future profitability may rely more than ever on learning from the lessons of FY 2021 and capitalising on the best takeaways. A growing penchant for similar commissions and inquiries, however, may drive additional growth opportunities in the future.

Much as the American astronauts learned that they were able to do things they never dreamed possible through seemingly countless climb-and-dive cycles in their aircraft, how Australia’s largest law firms learned to navigate FY 2021 will provide important insights into how these firms may successfully confront what lies ahead.

METHODOLOGY:

Financial metrics are derived from aggregated data collected by Thomson Reuters Peer Monitor from the financial management systems of 16 participating law firms operating in Australia, including some of the largest firms in the region by lawyer count. Global metrics are based on aggregated data from 170+ Peer Monitor participating law firms and their operations in the United States, United Kingdom and Asia.

Also, client insights included in the report were based on interviews with Australian legal buyers over the course of financial year 2021, provided from Thomson Reuters’ Market Insights. This product provides legal buyer information from around the globe from annual interviews from 2,500 legal buyers with revenues above $50 million (US).

Finally, partner movement data is based off the rigorous research and tracking over the course of FY 2021 by legal consultancy firm, Alpha Creates.

1 Profit as percent of Revenue (G/L) – G/L Revenue minus all expenses (Direct and Indirect) divided by G/L Revenue

2 For purposes of this report, demand is defined as average total billable hours worked by law firms during a specified period.

3 Qualified Fee Earners refer to practicing lawyers. Titles included are associates, senior associates, equity and non-equity partners, of counsel, and other lawyers.

*Thomson Reuters gratefully acknowledges the participation of the following persons in the preparation of this Report: from Alpha Creates – Eric Chin, Principal; from Barolsky Advisors – Joel Barolsky, Managing Director; and from Thomson Reuters – William Josten, Manager of Enterprise Legal Content – Thought Leadership, Isaac Brooks, Analyst – Peer Monitor, Bryce Engelland, Industry Analyst, and David Johnson, Senior Client Relations Manager.

A closer look at market forces

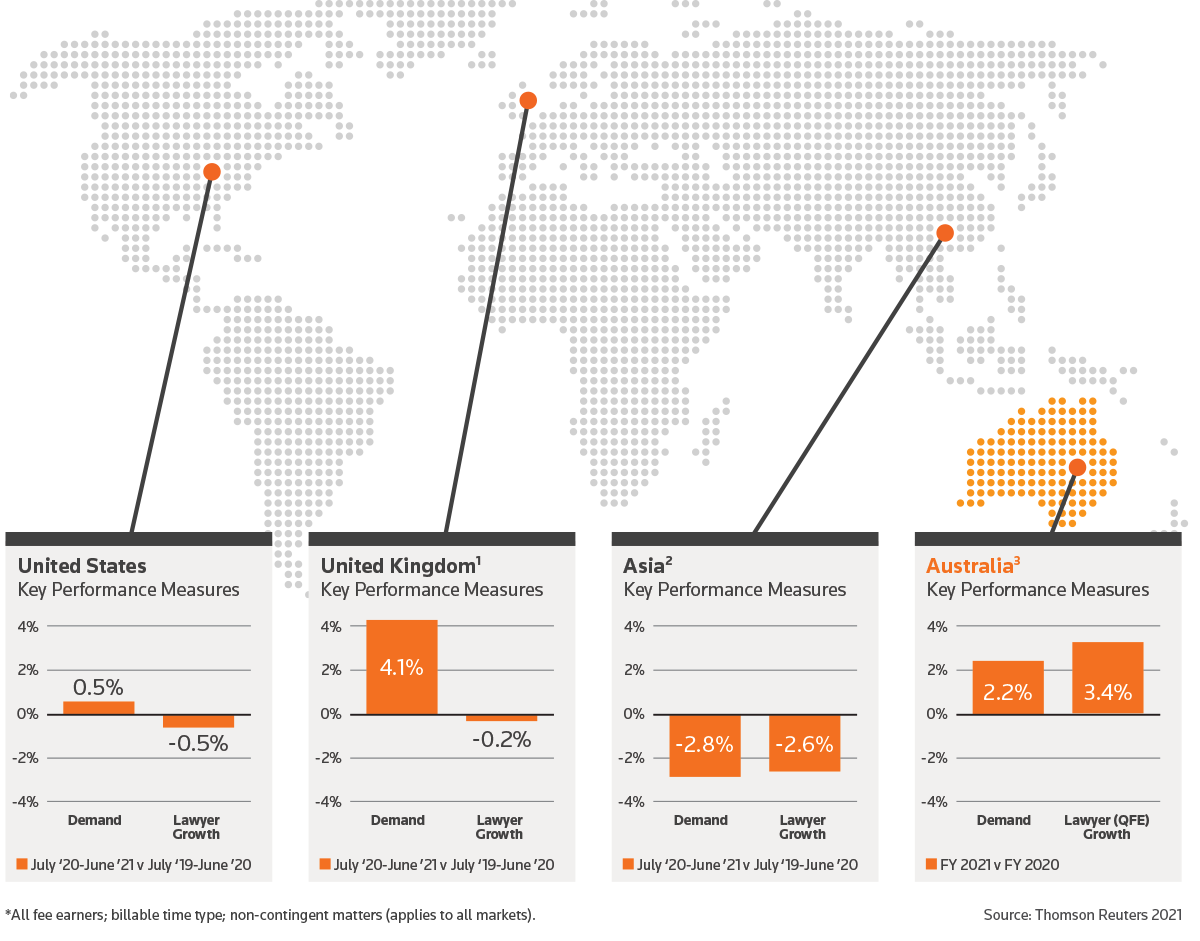

Figure 1 – Global Growth Metrics – Last 12 Months

For the most part, global legal demand for legal services over the past 12 months has been better than many industry observers anticipated at this point last year. While the Australian market has led growth in global billable hours in recent years, this past financial year was a step back from that historic pace. Regardless, Australian law firms trailed only the U.K. market in terms of demand performance, mostly because law firms experienced a busy six months following the official start of Brexit.

Australian firms did see overall average demand growth that was four times the pace of the average U.S. firm. And while many Australian law firm leaders have been tepid about their future prospects compared to recent years, they remain relatively optimistic globally as reflected in the higher-than-average performance in Lawyer or Qualified Fee Earner (QFE) growth over the past 12 months. Conversely, U.S. law firms are, on average, at slightly lower levels of staffing both within the U.S. operations as well as their U.K. offices; many are also seeing deeper contractions, especially in their Asia operations.

Key performance metrics for Australian law firms

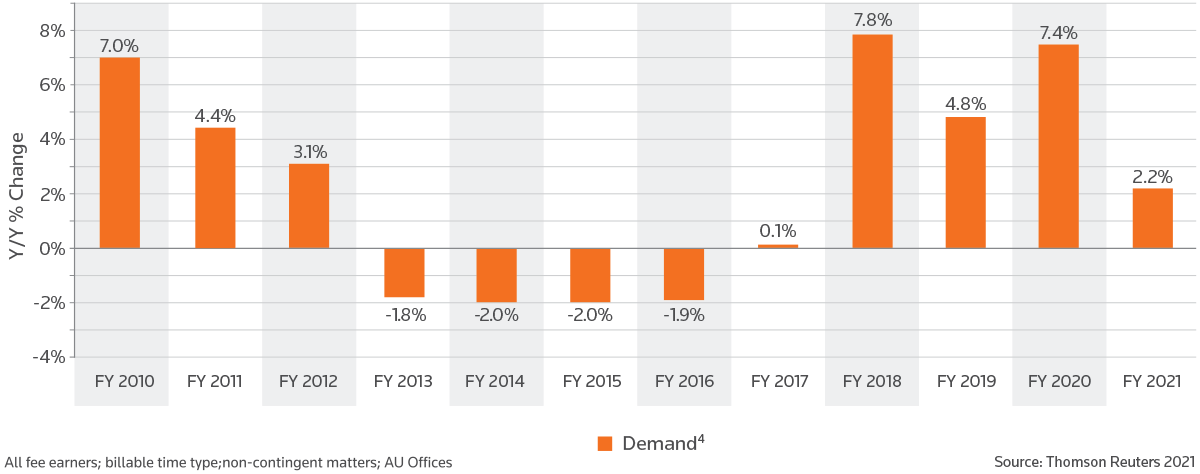

As mentioned, the average Australian law firm ended FY 2021 with 2.2% increase in legal demand. This is a low point from the marks set in previous years where these same firms saw an average growth of 7.8% in FY 2018, 4.8% in FY 2019, and 7.4% in FY 2020.

Figure 2 – Historic Demand Growth

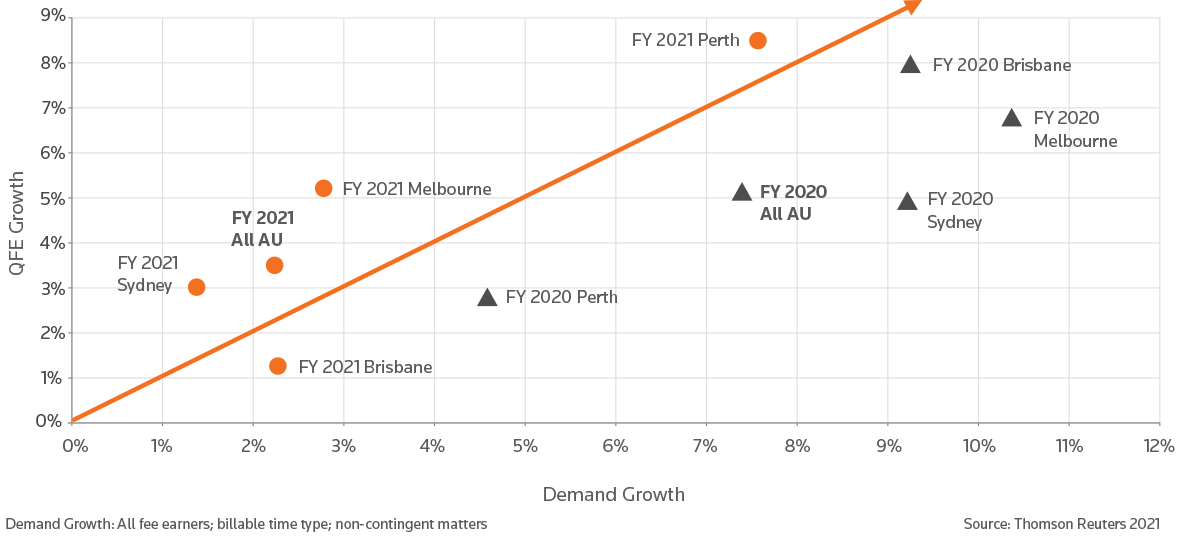

The slowing of growth looks to be very broad-based with respect to key geographic locations. Only Perth outpaced the demand growth figure posted for FY 2020. Perth, which was a relative laggard in FY 2020, now leads major markets with 7.6% average demand growth and 8.5% average QFE growth. Brisbane (14%), Melbourne (27%), and Sydney (45%), which account for 86% of the billable hours tracked in the sample, all saw their FY 2021 figures fall below the pace each set in FY 2020.

Figure 3 – Markets Matrix – FY 2021 & FY 2020

Another reason for the slower demand growth of FY 2021 relates to dispute resolution matters, one of the major drivers in the legal market overall, representing 22% of all hours worked. After a couple of strong years, growth in that practice area fell to just a 1.9% average increase.

Indeed, among the top growth practices in FY 2021 are transactional and corporate practice areas, helping to make up the slowing pace of disputes. Further, regulatory matters — one of the smaller practice areas tracked, but not normally featured — saw market-leading growth of 14.8%. Growth in regulatory work was driven in part by aggressive regulators, Foreign Investment Review Board reforms and growth in mergers and acquisition (M&A) matters requiring approvals.

M&A work was another pocket of success during FY 2021, growing by 9.4% on average. After Q1 FY 2021 when the pandemic still provided plenty of uncertainty, corporate deal work began to ramp up in each successive quarter, culminating with 23.1% average demand growth in Q4 of this financial year. Globally, other legal markets saw similar trends with regard to their M&A practices, albeit to lesser degrees.

With the exception of regulatory and M&A work, many Australian law firms experienced slower relative growth in each of the other major practices in FY 2021 than what was seen during FY 2020.⁵ The broadbased nature of slower demand growth by both geographic location and practice areas accounts for the slower pace of overall demand growth for the year.

Figure 5 – Key Performance Measures⁶

Finally, looking more broadly at the other key performance indicators, we see that the slower demand growth is a primary driver of slowing fees worked, which serves as a proxy for revenue. Fees worked still grew by 3.6%, but at less than half the pace in FY 2020 (8.5%).

Utilisation fell into negative territory as demand growth did not match the pace with which QFEs were added in FY 2021. This trend completes the story shown in Figure 3, with all the geographies, except Brisbane, shifting from the right side of the orange line, representing a one-to-one ratio between the demand and QFE metrics, to the left side of the line in FY 2021.

1 Based on US-based law firms activity in the United Kingdom.

2 Based on US-based law firms activity in Asia.

3 Based on Australia financial year of July – June.

4 Billable time type: Non-contingent matters means that all contingent work has been excluded from the pool of hours measuring demand.

5 It should be noted that Construction work did perform better in FY 2021 than in the previous year, but still saw overall practice demand decrease, creating a situation where it was less negative than the previous year, but still negative, nonetheless.

6 Key Performance Measures: Defines the rate of change from the stated period to the same period 12-months earlier; includes values from all fee earners (i.e., firm-employed qualified fee earners (QFEs) [lawyers], other professional fee earners [paralegals, legal secretaries, etc.], and contractors) Demand: Total hours worked. Worked Rates: Reflects hourly rate after negotiated discounts from the Standard/Rack Rate. Fees Worked: Worked Rates multiplied by Demand. Utilisation: Hours worked by all fee earners divided by qualified fee earner full time equivalents (FTEs) QFE growth: Total Qualified Fee Earner (lawyers) full time equivalents (FTEs)

Talent trends

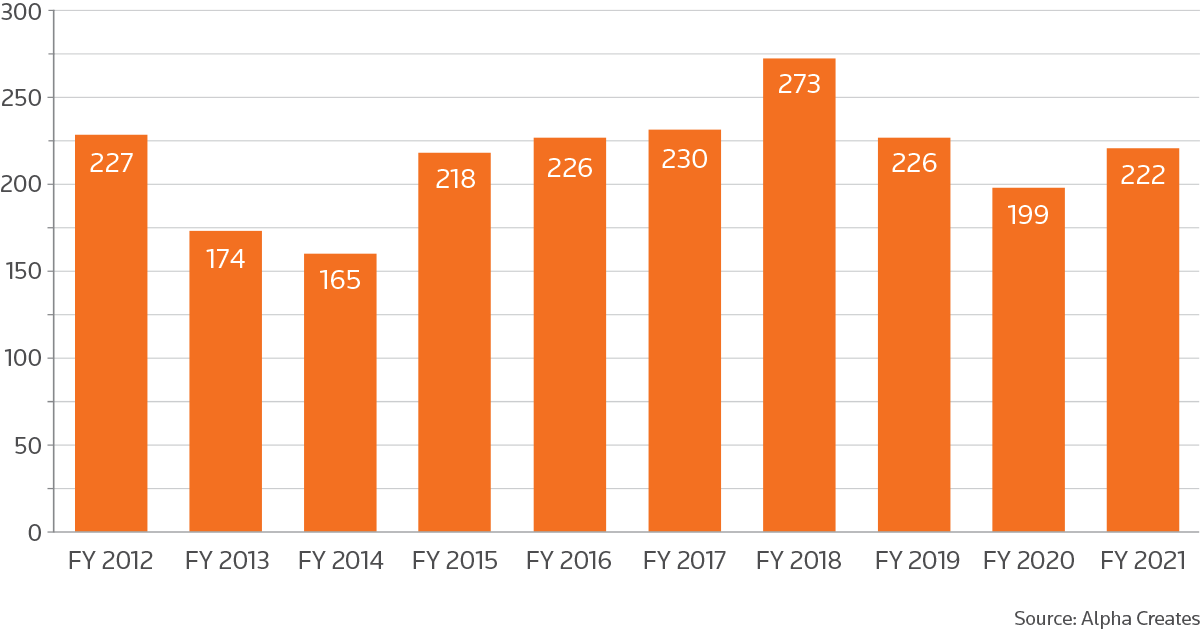

Declining utilisation was not the only interesting aspect when it came to talent trends. Analysing the movement of partners in the legal industry can reveal how firms have strategised to grow. Alpha Creates’ annual tracking of law firm partner movement in the Australian legal market reveals partner mobility has nearly recovered to pre-pandemic levels. In all, 222 partners switched firms in FY 2021.

Figure 6 – Number of Lateral Partner moves by Financial Year

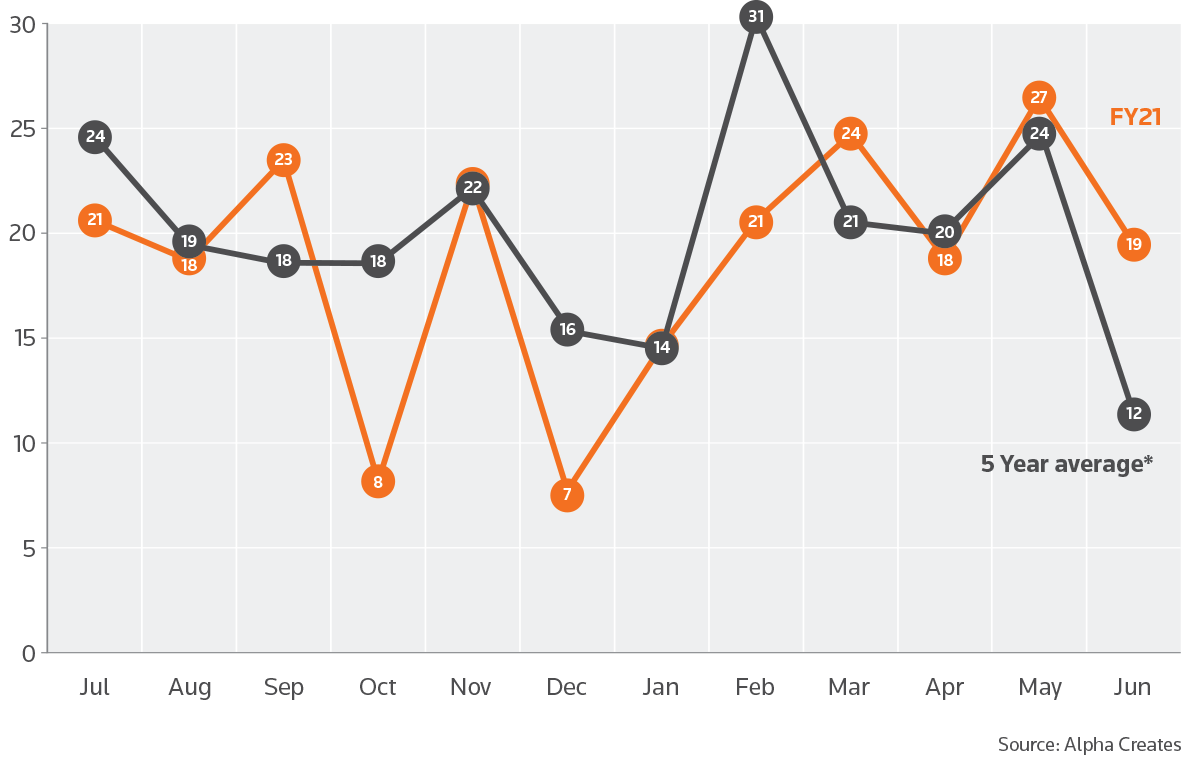

A comparison of partner movement by month in FY 2021 against the previous five-year average reveals some volatility in partner movement in FY 2021 as the industry recovered from the pandemic low of FY 2020.

Figure 7 – Number of Lateral Partner moves by month

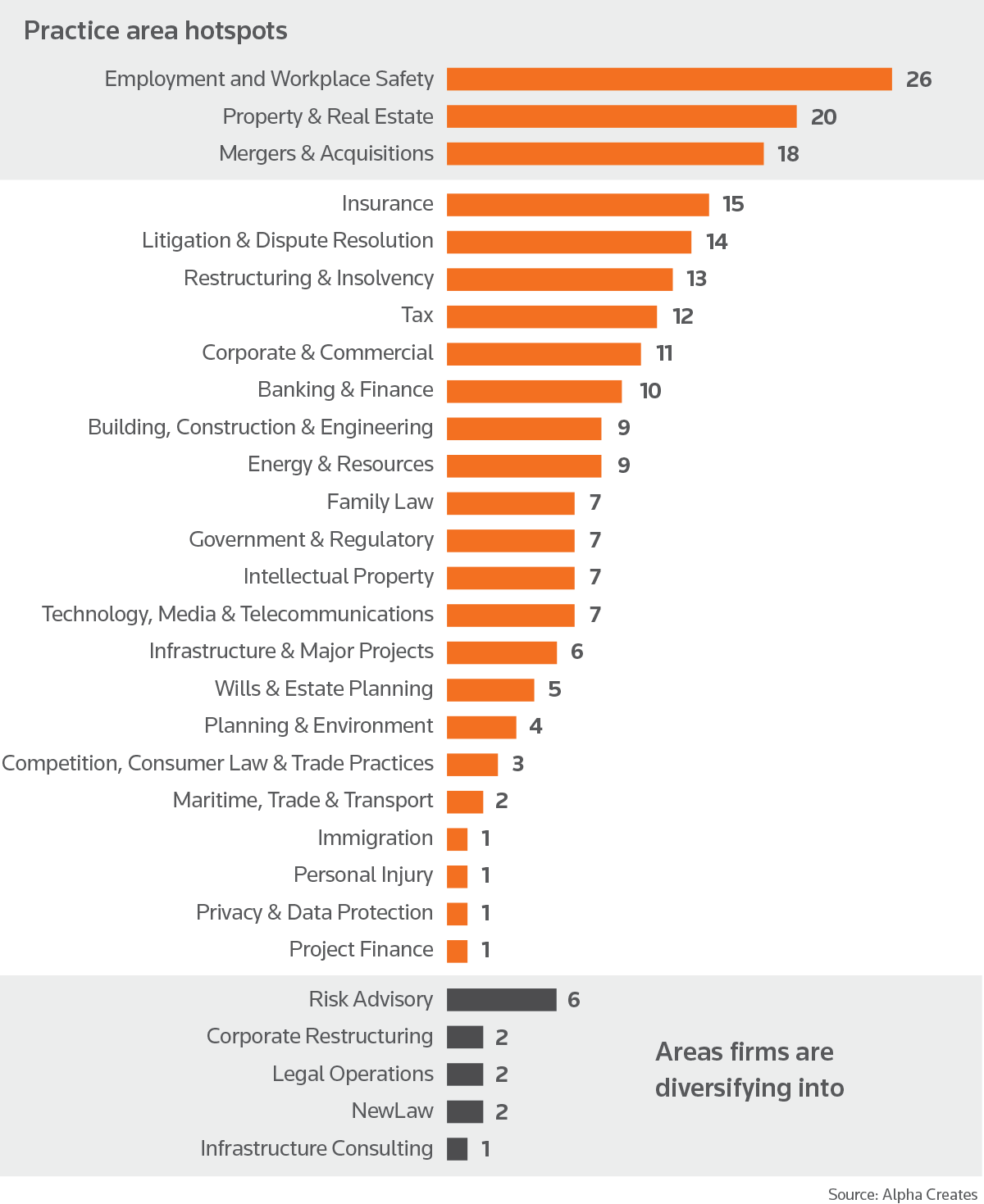

A deeper dive into this data by practice area reveals that firms added lawyers in employment and workplace relations as Corporate Australia turned to its lawyers for advice on work-from-home policies, and COVID-19-safe compliance with state and federal government guidelines. In addition, property & real estate, and M&A were also competitive hotspots for partner talent.

Figure 8 – Practice Breakdown of FY 2021 Partner Movements

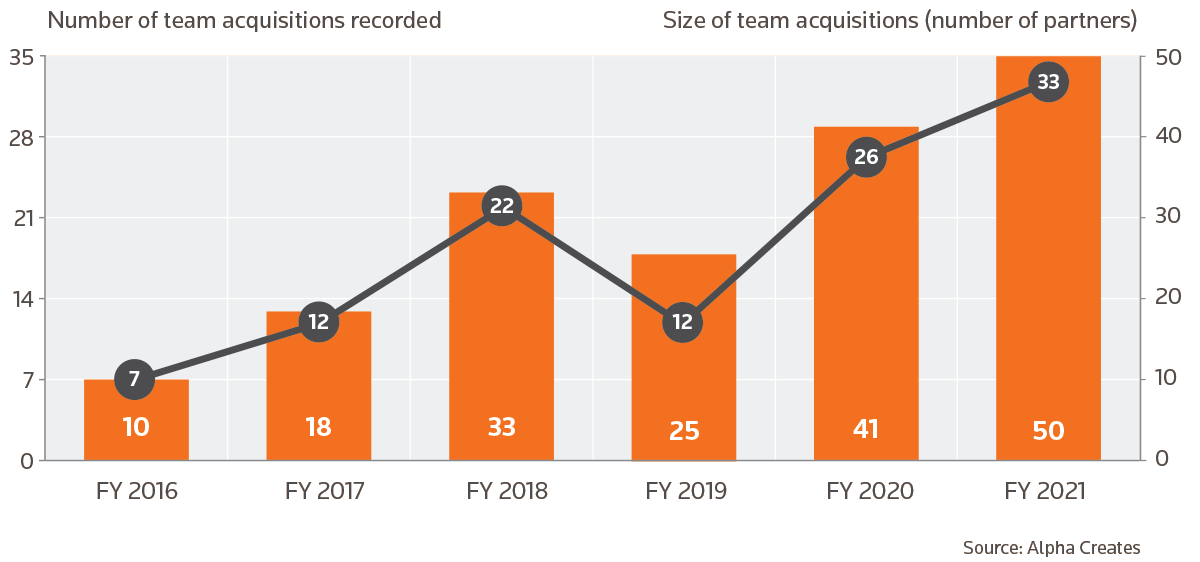

The trend towards team acquisitions continues to shape the war for talent in the Australian legal industry. Fifty partners switched firms as part of a team of lawyers, making this the highest number of partners to move across with their teams since Alpha Creates began tracking this data in FY 2016.

Figure 9 – Number of Partner Team Acquisitions by Financial Year

Thomson Geer was the most active team recruiter, with five team acquisitions that brought in 12 partners plus their teams. Mills Oakley, Squire Patton Boggs, and Wotton + Kearney each recorded two team acquisitions that brought in three partners apiece. Notably, U.K. law firm Watson Farley & Williams is the latest international law firm to land in Australia, launching its Sydney office with a team of partners hired from Withers in March 2021. Kennedys also launched its Perth office by acquiring a team from Clyde & Co. in May 2021.

Globalisation also contributed to shaping the Australian legal landscape in FY 2021, with 17 international law firms gaining 59 partners through the lateral market. Ashurst was the most active, with 17 partner level recruits joining its legal practice, consulting, and managed legal service businesses, followed by Dentons (seven partners) and Squire Patton Boggs (six partners).

NewLaw firms⁷ and alternative legal service providers have also remained active in FY 2021. Keypoint Law continued to add law firm partners to its ranks, gaining seven consulting principals through the lateral market. Nexus Law Group, meanwhile, expanded its footprint in the Adelaide and Perth markets with lateral hires.

Further, law firm competitors also took advantage of the accelerating lateral market to acquire new talent. The Big Four accounting firms’ legal arms grew their practices through lateral hiring, with KPMG Law adding three partners, and EY Law adding two partners in FY 2021. Of note, midsize market accounting firm Bentleys also launched Bentleys Legal through a lateral hire from Dentons.

7 NewLaw Firms: Term describes a burgeoning category of alternative legal service providers that sets itself apart from BigLaw or TradLaw providers in the following key ways: Using new or “disruptive” technologies, encouraging flexible working, and offering alternative pricing strategies.

The shifting workload and its impact on profitability

Last year’s report stated that in Q4 of FY 2020 (the first full quarter of the pandemic’s effects), partners were in high demand from their clients and produced on average of nine more billable hours per QFE, per month. At that same time, we saw associate work step back along with work done by other professional fee earners⁸ (OPFE) to roughly equal degrees, proportionally. Over the past 12 months, however, these statistics have evolved considerably as law firms continued to see an above-average share of work still being done by partners, even though this has tailed off in recent months. To balance this shift, associate proportions recovered and even surpased levels seen before the pandemic.

It is possible that technology and remote working may have reduced the need for OPFE, contributing to a 2.3% reduction in the portion of billable hours for these titles in FY 2021 compared to FY 2020, a figure which takes on a massive impact when calculated across the millions of hours and fees impacted.

However, law firms may have had the better of this shift, at least in FY 2021. The average hourly rate for OPFE is $246. In contrast, the average lawyer worked rate is $487. The shift in hours from OPFE to lawyers effectively changed the blend of the rates charged across the market, contributing to the “All Fee Earner” worked rate growth seen back in Figure 5.

As you can see on the right side of Figure 10, “Lawyer Only” worked rates grew at a slower rate than either FY 2019 or FY 2020, finishing FY 2021 up only 0.2%. This is a strong indication that firms didn’t aim to increase their lawyers’ price-per-hour to the degree that the “All Fee Earner” worked rate growth figure would suggest. In previous years, the increase in “All Fee Earner” worked rates was driven by realdollar increases in lawyer worked rates. In contrast, the growth in this figure in FY 2021 was due to the proportional shift of work up to higher-cost lawyers rather than actual real-dollar increases, potentially reflecting a response by law firms to clients’ demand for greater consideration to the economic and business fallout from lockdowns throughout the country.

Figure 10 – Shifting Workloads impact on Worked Rate Growth

8 “Other professional fee earners” refers to timekeepers including paralegals, litigation support staff, specialists, summer associates, and other fee-earning professions.

Expenses, revenue and law firm profits

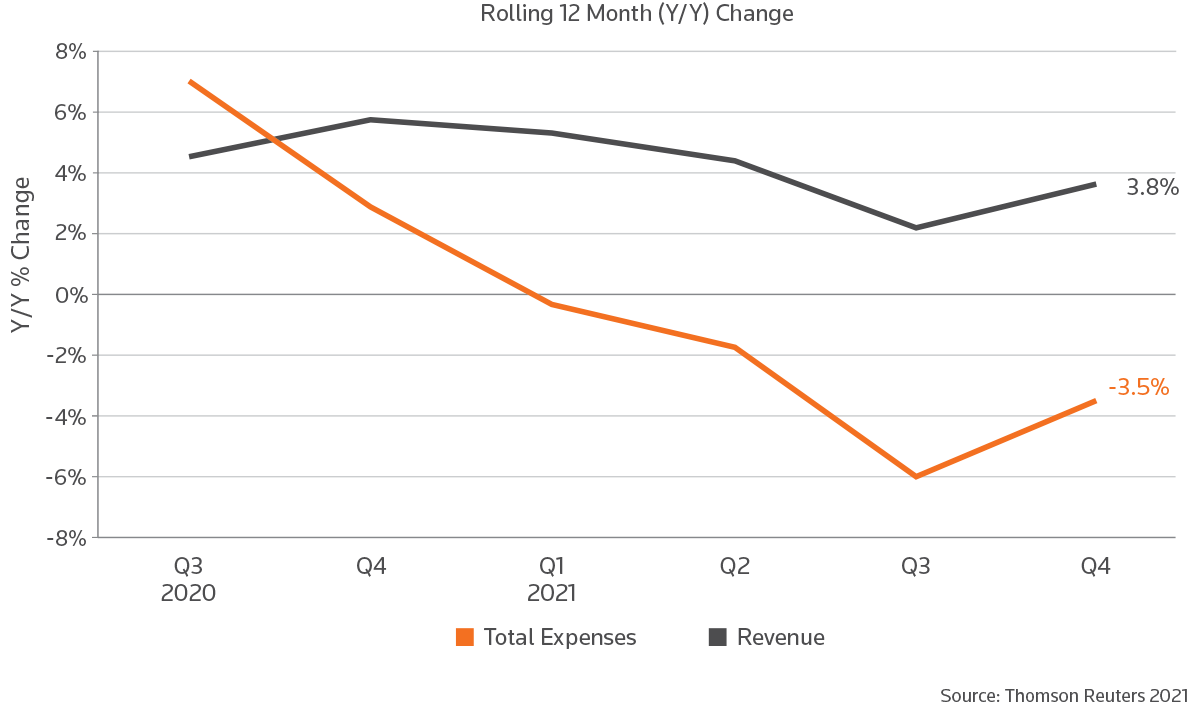

Figure 11 – Expenses & Revenue Growth⁹

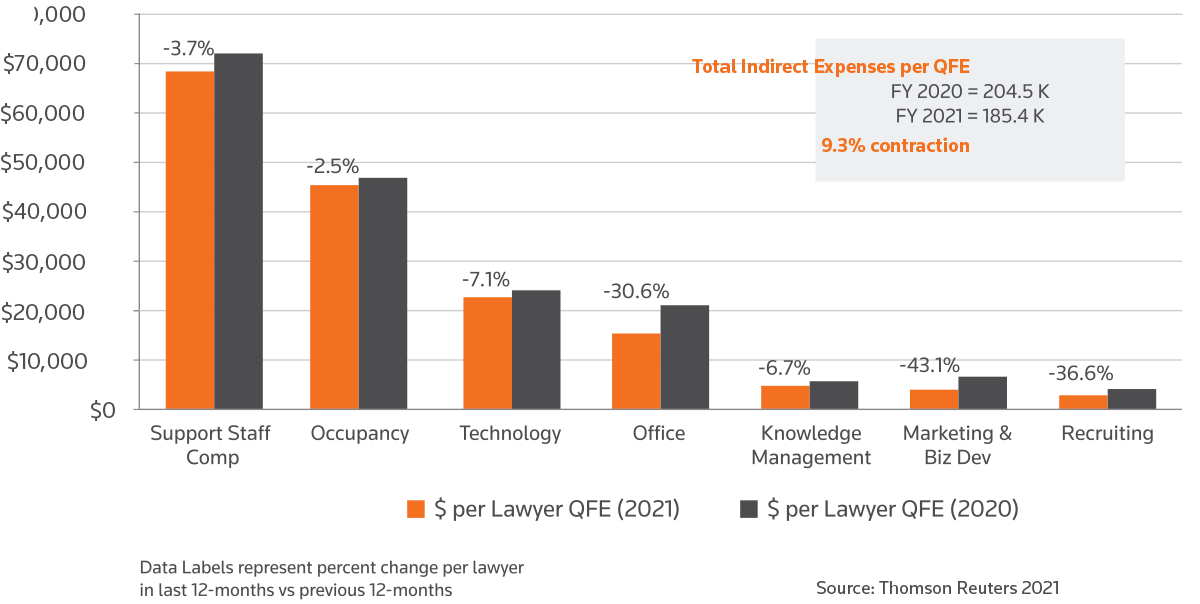

As noted previously, Australian law firms were able to reduce overall expenditure by 3.5% in FY 2021, due largely to pre-emptive measures taken in 2020 and savings realised from the necessary shift to remote working and other factors related to the pandemic. This marks a sharp reversal from Q3 of FY 2020 (the last full pre-pandemic quarter), when the average law firm increased overall expenses by 6.9%.

In FY 2021, a large majority of those expense reductions came from the indirect expenditure, which declined by 9.3% per QFE on average. Indirect expenses in this report represent all law firm expenses except compensation and benefits for lawyers and other fee earners. About 45% of all indirect reductions came from office expenses, which includes items such as pens, paper, furniture, or anything not included in rent payments, as well as marketing and business development spending. The figures also show that non-billing support staff compensation was another area of likely reduction. The indirect expense category that saw the least amount of contraction percentage-wise was occupancy, which is likely due to rent increases that were built into leases which long pre-dated the pandemic, and which will likely be a source of close examination by law firm leaders going forward.

Figure 12 – Indirect Expenses per QFE

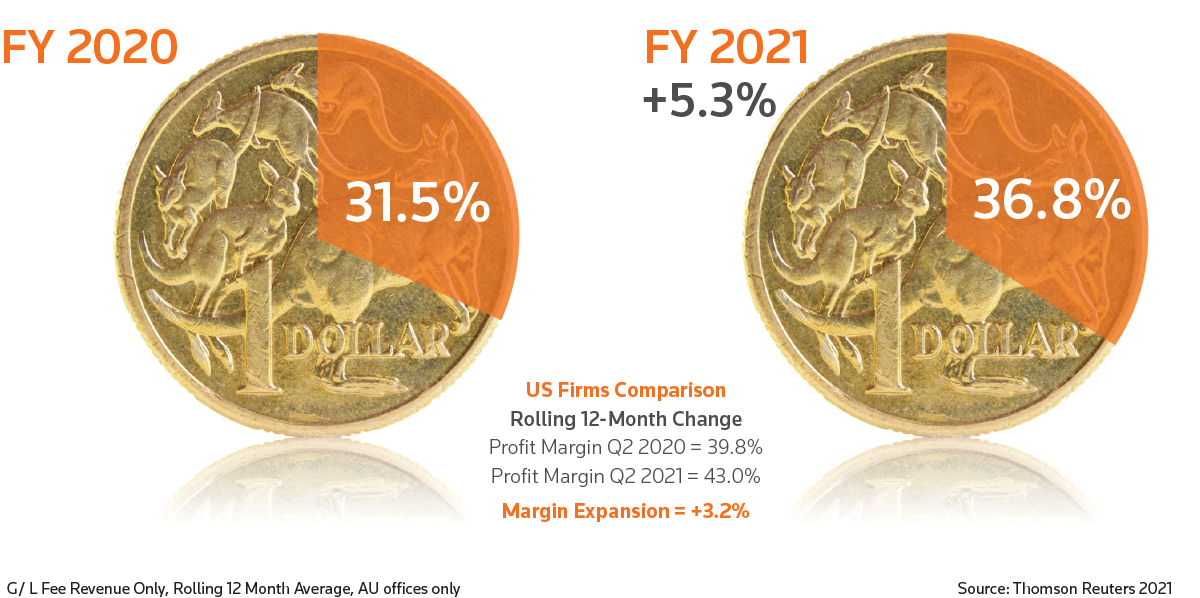

While top line revenue grew at a slower pace than previous years, the 3.8% average growth posted for FY 2021 matched inflation.¹⁰ This revenue performance, along with the shift of expenses from growth to contraction, bolstered profitability metrics over the past year. Average profit as a percent of revenue at the end of FY 2020 was at 31.5%; and grew to a notably strong 36.8% for FY 2021. Law firms in the U.S. similarly saw strong growth in their profit margins, but to a smaller extent.

Figure 13 – Average Profit as a Percent of Revenue

9 Expense, revenue, and profitability results are reflected on a rolling 12 months basis to annualise heavy expense quarters (i.e., Q4 2021 contains data from July 2020 thru June 2021) Total Expenses includes both Direct and Indirect Expenditure.

10 Per the Reserve Bank of Australia, “[h]eadline inflation has continued to be affected by government subsidies and rebates as well as other one-off effects, and increased by 3.8 per cent over the year to the June quarter.” Statement of Monetary Policy, August 2021. https://www.rba.gov.au/publications/smp/2021/aug/inflation.html

Clients’ view of law firms in FY 2021 and beyond

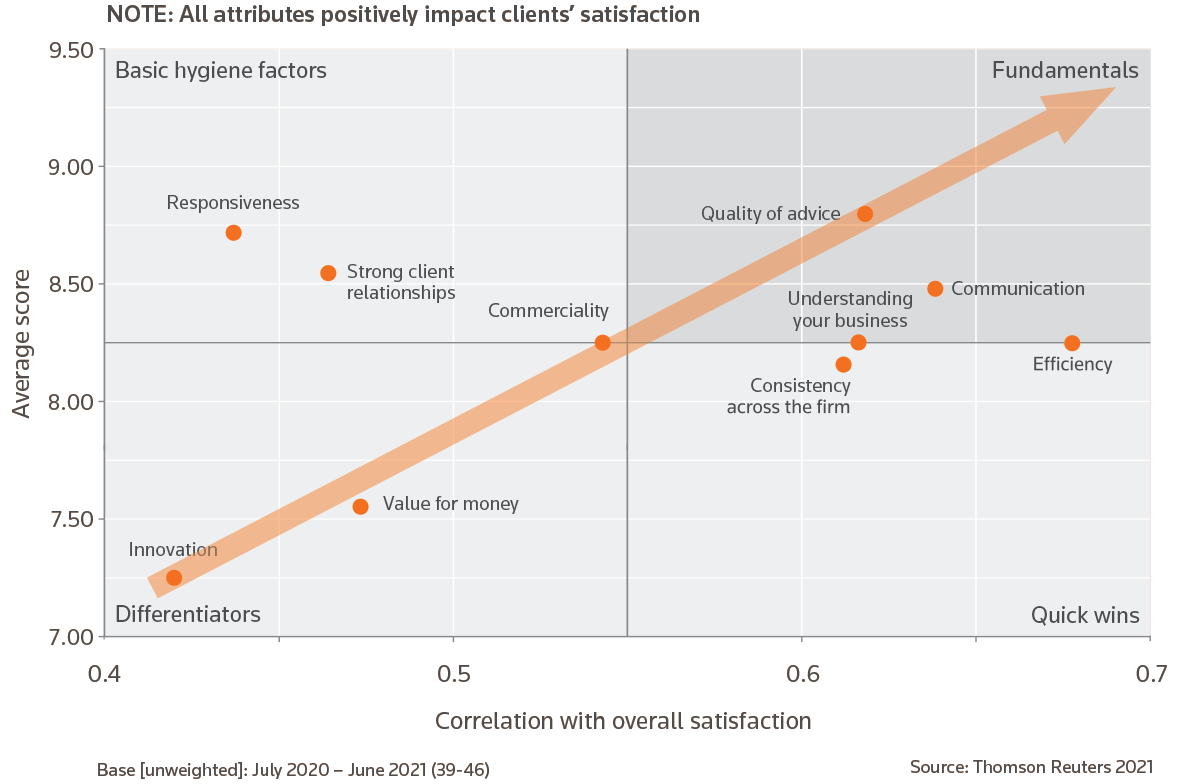

Figure 14 – What areas of service underpin satisfied clients? – FY 2021

Now, let’s change gears and look at the key drivers of client satisfaction in the Australian legal market. The chart above provides insight into what is driving satisfaction among clients of Australian law firms, and the data shows the correlation between different elements of service delivery, with the ultimate satisfaction the client expresses with their outside law firm.

The findings demonstrate that a law firm’s quality of advice, strong communication, business understanding, and efficiency were the key attributes that most closely correlated with satisfied clients.

Indeed, the data underscores that the effect of efficiency, relative to value for money, in driving overall client satisfaction suggests that clients are moving to a place where they appreciate and value the efficiency with which firms deliver quality results. This shows that the key to maintaining satisfied clients lies in the ability to demonstrate that work is being delivered as efficiently as possible.

Figure 15 – “Stand out” skills identified by clients

Figure 15 above provides similar themes, with a vital difference. For this figure, in-house leaders were asked specifically about traits exhibited by those external lawyers whom the client identified as truly standing apart from the crowd, their “stellar performer” lawyers.

This demonstrates that the legal market is responding most favorably to the outside lawyers who can combine technical knowledge with a forward-looking, commercially attuned mindset to deliver the best advice in an effective manner. Overall, it is clear that there are additional benefits to be gained by upskilling and focusing on professional development within law firms in these areas. The end results might be the determining factor in a firm’s ability to win work and create beneficial, long-lasting relationships.

Clients’ view of law firms in FY 2021 and beyond

Many of those same outside lawyers who combine technical and commercial acumen are also those who are best positioned to help their law firms reimagine how legal services are delivered.

Innovation is becoming a permanent part of law firms’ strategy and structures. According to Alpha Creates’ study of the state of legal innovation in the Australian legal market, 30 of the 50 largest law firms in Australia have now formalised an innovation function. A majority of these innovation duties within the firms surveyed have been allocated to existing roles, meaning that partners, knowledge management directors, and heads of technology are being asked to take on the additional role of

leading innovation. This is an opportunity for dual-mindset lawyers to really set themselves apart.

Figure 16 – Number of firms with a formalised Innovation function

Dedicated innovation roles within law firms are still relatively new due to a combination of resource and feasibility constraints. Lawyers who take on these innovation roles have to balance their billing targets and new strategic innovation projects for the firm. However, the benefits of these roles can already be felt in the market as strategic innovation projects have helped firms transition seamlessly to remote working by digitising client interfaces and optimising workflows.

Legal innovation means different things to different firms and organisations, of course, and it falls across a spectrum that ranges from law firms’ internally focused innovation, such as digital transformation and legal project management, to more client-facing innovation, such as client portals and legal operations consulting arms, and market-facing innovations, such as legal tech incubators and accelerators.

The “headwinds” and “tailwinds” for today’s law firms

This report opened with reference to a somewhat obscure aircraft and the tribulations to which it exposed its passengers. To further illustrate the forces that are pushing Australia’s law firms forward and those that are holding them back, perhaps we should shift to a more relatable aircraft illustration.

The successful operation and timely arrival of any airplane, including the largest commercial airliners, depends on the successful balancing of tailwinds, headwinds, and the internal operations of the aircraft, such as the engines and crew.

The managing partner of a large law firm can be thought of as the captain of a large commercial airliners, ultimately tasked with the responsibility of balancing these often divergent forces while maintaining order in a complex environment.

Despite the turbulence around them, most law firms (the aircraft in our analogy) have continued to increase their revenue trajectory following some initial bumps in the prior financial year, and profits have followed suit.

The key question is, will it continue?

Let’s address this by looking at the major forces at play — again, the tailwinds, headwinds, and internal operations.

TAILWINDS

Liquidity in the broader market — Many large commercial law firms are enjoying the impact of the second round of cheap, abundant capital. There seems to be an almost unlimited supply of money looking for a good home. The cost of debt and equity are at all-time lows, and money is flowing from super funds, private equity, family offices, and a range of other sources.

Capital market liquidity generally means more public and private M&A, more property deals, more equipment purchasing, and so on. All of this drives legal work, both for corporate and finance lawyers, but also for a range of complementary practices.

Infrastructure investment — According to Macromonitor,¹¹ there are more than $100 billion worth of transport infrastructure projects currently underway in Australia, with more in the pipeline. Federal and state governments have realised that deficit is no longer a dirty word and are committing major funds to social and public infrastructure projects. Some of this spending, of course, is aimed at mitigating any long-term negative impact of the pandemic on employment and economic growth.

While infrastructure investment is great news for construction companies, there is also a large amount of legal work required before, during, and after each of these major projects. This is likely to keep construction litigators very busy.

Government policy — There has been the increasing number of royal commissions, government reviews, and inquiries in recent years. Governments of the day seem to prefer to use of these processes to address politically sensitive matters and to initiate new public policy.

This trend is proving to be a field day for many law firms, clearly illustrated by the impact of the Hayne Royal Commission investigation into the banking sector. More recent enquiries into aged care, police informants, Crown, mental health, and the disability sector have not been of the same scope and scale of Hayne, but they have been very lucrative for the law firms involved.

One of the by-products of these commissions and inquiries are class actions by disaffected consumers, shareholders, or other stakeholders. Defending these claims is another positive driver of legal work.

Data and digitisation — Sydney Business Insights¹² recently stated that 90% of the world’s data was created within the last two years. Not only is the data universe exploding but the pandemic accelerated the pace of e-commerce and e-service delivery for almost every public and private sector organisation.

While this trend is a boon for technology companies, there are also spin-off benefits for law firms that provide advice in:

- commercialisation of data, data analytics, and privacy

- data governance

- technology transformation and outsourcing

- artificial intelligence development and deployment

- cloud contracting and the internet of things

- cybersecurity

- telecommunications services and technology infrastructure and

- development and use of blockchains.

Decarbonisation — The 2021 Davos Agenda listed the world’s top risks by likelihood and impact. Five of the top 10 risks related to climate change and environmental sustainability. The shift to renewable sources of energy seems inevitable, and there will be an abundance of legal work associated with restructuring the energy sector. Also, there will be a need for legal advice around managing “green” risk and compliance with new environmental regulations.

Social license preservation — There have been a number of recent case studies that showed major companies that have lost trust amongst their key stakeholders and the broader community due to poor ethical behaviour. Maintaining a social license to operate has become a major strategic issue for large and small enterprises, as well as for non-profits such as schools and religious organisations.

This concern is driving legal work because many organisations are reviewing their current practices to ensure that they are compliant with the law and with meeting community expectations.

Wealth transition — Roughly 56% of Australia’s private wealth is currently held by people aged 56 and older. More than AU$3 trillion of this wealth will have to change hands over the next 20 to 30 years. Given this and the potentially large number of recipients and a more complex array of assets to divide up, the demand for succession and estate planning will only increase.

HEADWINDS

The lingering effects of the pandemic — The number one risk to the Australian legal market is the potential headwind of a largely unvaccinated community paralysed by frequent lockdowns and border closures, both interstate and international.

On 2 July 2021, the Morrison Government announced a four-phase plan to return to “COVID Normal.” If the snail-paced vaccination rates continue as they are, however, we may only reach Phase 2 by the second quarter of 2022 and Phase 4 in 2023. Indeed, recent lockdowns across the country illustrate the challenge in progressing through the various phases. A prolonged period before reaching Phase 4 is expected have significant implications for the country’s broader economy and its law firms.

Brain drain — As things stand, the U.K., the U.S., and other legal centres may return to a relatively normal state as much as 12 months ahead of Australia. Many ambitious, talented young Australian lawyers will see major benefits by working and living abroad. Talented expats may be unable and unwilling to return home.

The lure of London is likely to be even more compelling than usual — the ability to do great work, earn good money, live without lockdowns, and put your passport to good use might be too much of a lure for some Australian lawyers. Unfortunately, this brain drain will hit Australia’s law firms when these resources are needed the most and Australian firms have few viable alternative plans.

A depressed commercial property market — The recent lockdowns and border closures resulted in a significant drop in demand for commercial properties, hotels, and high-rise residential real estate. Should this continue, a depressed property market will directly impact real estate lawyers and could also affect other areas like construction, banking, and project finance.

Collapse in travel, tourism & education — The government-support packages and insolvency moratoriums that began in April 2020 have kept most businesses in the travel, tourism, and education sectors alive. A dramatic rise in domestic tourism has helped offset some losses associated with fewer visitors; but as the lockdowns continue, a vast majority of these businesses are too small to save. Eventually the liquidators will move in, which may be good news for law firms’ insolvency practices, even if it negatively impacts the broader economy.

INTERNAL OPERATIONS

The managing partner, or airline captain, mentioned above cannot control all of the tailwinds and headwinds his flight faces, only how they are navigated. But a captain does control the aircraft itself — how the engines perform, how the plane operates, and what flight path it takes.

Four engines — Two of the most iconic aircraft in history, the Boeing 747 and Airbus A380 were each propelled by four engines. One can conceive of our law firm, or aircraft, as similarly being powered by four distinct engines:

- Ability — the technical legal skills and know-how to solve client problems, provide advice, and create client value.

- Affinity — the capability to develop strong client relationships and a positive emotional connection with the firm’s brand.

- Stability — the spirit and cultural dynamics of the firm that keeps everyone engaged, loyal, and collaborative.

- Efficiency — the ability to produce quality work with optimum resource use and capture value through a seamless client experience.

To successfully manage these four disparate yet inextricably interrelated engines, firms are fostering the rise of legal operations functions.

The fourth engine mentioned above — efficiency — is still very much a work-in-progress at many Australian law firms, even as this area becomes more important as bargaining power shifts to clients. With this power shift, law firms are realising that they need to become more adept at capturing and conveying value to retain their key client relationships and thus, their margins.

A robust legal operations function is emerging as the strategic response to this need.

The below diagram attempts to map the legal operations arena in law firms. Though visually complex, it illustrates how many existing functions — such as lawyering, legal administration, knowledge management, legal technology, pricing, finance, and innovation — must interconnect to make this engine of law firm propulsion more powerful. And it’s possible, even likely, that while already complex, this graphic may well be an oversimplification of the process.

Figure 17 – Mapping Legal Operations

11 https://macromonitor.com.au/transport-infrastructure/

12 https://sbi.sydney.edu.au/megatrends/impactful-technology/

13 CX represents Customer Experience

CONCLUSION

Whether one chooses to view the current state of Australia’s legal market as a rollercoaster, a large airliner, or a combination of the two hurtling astronauts through their training, the focus must remain on the continuing pressures being applied across the Australian legal landscape and the forces which will continue into the future.

Many of these forces are beyond the control of law firm leaders, but those leaders will nevertheless be required to navigate them with skill and vision.

For those factors within law firms’ immediate influence and control, firm leaders must remain vigilant and continuously push for greater innovation while carefully managing the “engines” that drive their firms forward. Despite successful years, including a surprisingly positive FY 2021, no one should consider their law firm to be on “auto pilot.”

At the same time, the captains of today’s law firms should be feeling relatively content. The tailwinds appear to be much stronger than potential headwinds; yet we must remain aware of potential thunderstorms on the horizon.

That said, firm leaders need to work especially hard to get efficiency —their fourth engine — to work as well as the other three, without losing focus on firm performance. Efficiency is the weak link in the chain.

Much progress can be made on this front through a committed development of and investment in legal operations and innovation. Such progress requires help from the whole crew, as long as leadership is actively listening to what their clients are saying.

This may all seem like a lot to balance, but for better or worse, it’s exactly the type of leadership challenge that comes with the job.

Happy flying!

Thomson Reuters is a leading provider of business information services. Our products include highly specialized information-enabled software and tools for legal, tax, accounting and compliance professionals combined with the world’s most global news service – Reuters.

For more information on Thomson Reuters, visit tr.com and for the latest world news, reuters.com.

The Thomson Reuters Institute brings together people from across the legal, corporate, tax & accounting and government communities to ignite conversation and debate, make sense of the latest events and trends and provide essential guidance on the opportunities and challenges facing their world today. As the dedicated thought leadership arm of Thomson Reuters, our content spans blog commentaries, industry-leading data sets, informed analyses, interviews with industry leaders, videos, podcasts and world-class events that deliver keen insight into a dynamic business landscape.

Visit thomsonreuters.com/institute for more details.

Alpha Creates helps leaders build better businesses in the legal industry through innovation gigs, strategy engagements and technology projects. We deliver on-demand access to industry-leading legal innovators, strategists and technologists, accelerating legal innovation for all legal consumers, regardless of size.

For more information, go to alphacreates.com.

Barolsky Advisors is a leading management consulting firm with a deep understanding of the culture and complexities of professional service organisations, in particular, law, accounting, engineering and business advisory firms. The firm specialises in strategy formulation and implementation. The founder, Joel Barolsky, is a Senior Fellow of the Melbourne Law School and formerly a Principal of Beaton Research + Consulting.

For more information, go to barolskyadvisors.com.