Time to focus on your employee value proposition

1. Attracting talent without unexpected FBT

With Australia’s unemployment rate at its lowest level for more than 50 years, it is unsurprising that more than three quarters of Australian business leaders surveyed at the end of 2022 identified “talent acquisition, retention and re/upskilling to meet a more digitised future” as the number one challenge facing them today.[1]

Remuneration and reward professionals are leaving no stone unturned in the consideration of new benefit offerings (either on a cost neutral basis or on top of package) to hire and retain top talent.

An effective and robust salary packaging program can provide a better remuneration outcome for employees, on a cost neutral basis for the employer.

For benefits provided on top of package, as FBT is effectively levied at the highest marginal tax rate (47%), the benefits which generally deliver the most to an employee’s bottom line are those where either a partial or full FBT reduction or exemption applies.

If you haven’t reviewed your salary packaging offering in the last 12 months, there really is no time like the present. As a cost neutral way to increase your EVP, it’s a win win win

Consider introducing or expanding your salary packaging program

There are a wide variety of benefits which can be effectively salary packaged. Depending on the organisation and industry this may include novated leases, superannuation, car parking, self-education expenses, income protection insurance, donations, airport lounge memberships or remote area housing.

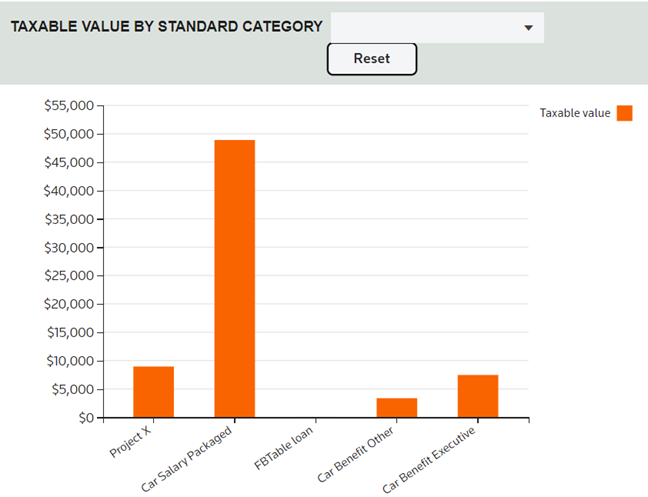

Standard Categories in ONESOURCE

Improving the standards of your reporting.

- Prioritise exemption caps treatments based on category creation and hierarchy

- Generate detailed reports providing specific insights on categories

- Interactive dashboard histogram that displays the 5 highest categories by taxable value (figure 1) and can be drilled down to the individual employee level (figure 2).

Figure 1

Figure 2

Check whether an FBT reduction or exemption can apply

There are a large array of FBT exemptions and reductions, however the criteria and documentation requirements need to be carefully considered to determine the likely FBT treatment of any new benefit offerings.

For example, recently many employers have sought to introduce or expand existing wellbeing programs. For these programs there are a variety of exemptions and reductions to consider (e.g. s58M exemption in respect of work relation medical examinations, medical screening, preventative health cat, counselling and migrant language training). However, depending on the nature of the proposed benefit and how it is provided, in some circumstances an FBT exemption may apply (e.g. flu or COVID vaccinations made available to all employees and administered by a medical practitioner) whilst in others it may not (e.g. reimbursement of an employee’s fortnightly gym membership expenses).

2. Electric Cars FBT Exemption

A new FBT exemption was introduced which can apply to zero or low emissions vehicles. ONESOURCE FBT has new functionality to assist with complexities surrounding this exemption.

- First held and used on or after 1 July 2022

- Have a value at the first retail sale (including GST) below the luxury car tax threshold for fuel efficient vehicles ($84,916 for FY23)

- Considered a car for FBT purposes (i.e. designed to carry a load of less than 1 tonne and fewer than 9 passengers)

- In respect of plug-in hybrid electric vehicles, the application or availability of the car was first committed to and provided as an exempt benefit before 1 April 2025

Importantly, the provisions allow for the relevant vehicles to be provided under standard novated lease and salary packaging arrangements.

Another important consideration is the commitment length for leased vehicles as a review of the effectiveness of the legislation will be undertaken after three years.

The key difference between this exemption and other FBT exemptions is that the grossed-up taxable value of the exempt benefit must still be included in the calculation of the employee’s reportable fringe benefit amounts. Consequently, there remains a potential impact on what is considered ‘income’ for certain government benefits and obligations (e.g. entitlement to the Child Care Subsidy).

ONESOURCE continues to pioneer the user experience in FBT preparation by automating the latest in legislative changes, saving you time and reducing your cost so your team can focus on what matters most.

Separately, the ATO is expected to release a draft practical compliance guideline in February, which provides a methodology to enable users of electric vehicles to determine an approximate cost for the electricity used when charging the vehicle at home. This amount may be relevant when calculating employee contributions or operating costs of electric vehicles.

Source:

Labor pledges tax breaks under revamped electric car policy (afr.com)

ONESOURCE FBT has functionality to ensure accurate RFBA reporting in respect of exempt electric vehicles. The car fringe benefits workpaper for FBT23 has additional fields allowing the user to indicate whether the car is an exempt electric vehicle. The taxable value of these vehicles will be included in RFBA calculations and reports but not in the FBT return.

FBT Treatment of exempt Electric Vehicles in ONESOURCE

Making exceptions easy as electing “yes”.

Figure 3: New "Electric/Fuel-Efficient Vehicle" exempt field in FBT23

ONESOURCE FBT has incorporated functionality to ensure accurate RFBA reporting in respect of exempt electric vehicles. The vehicle benefits workpaper and upload template for FBT23 has an additional field allowing the user to indicate whether the car is an exempt “Electric/Fuel-efficient vehicle”. By electing “Yes” as an exempt “Electric/Fuel – Efficient Vehicle”, the taxable value of these vehicles will be included in RFBA calculations, and any letters and reports generated but not in the FBT return.

Interested in what you’re reading?

Hear about the biggest changes in FBT this year.

3. Reduced FBT Record Keeping

In September draft legislation was released intending to reduce FBT record keeping compliance costs, together with two draft instruments outlining alternate documentation to travel diaries and the relocation transport declarations.

The legislation enables the ATO to publish legislative instruments permitting employers to rely on alternate documentation to substantiate reductions in taxable value than what is prescribed within FBT legislation.

The ATO has released two draft instruments in respect of travel diaries and relocation transport. These draft instruments propose to allow employers to collect the information required to substantiate a reduction in taxable value in alternate ways. The actual information required to be obtained remains unchanged.

While the changes to these two benefits will not be relevant to all employers, there is now a legislative mechanism in place and we anticipate further instruments in the future, so watch this space!

Instead of keeping travel diaries or relocation transport declarations, the drafts propose that other records containing the required information can be used such as employer and employee correspondence, corporate travel records, logbooks, expense management system records, other financial records/ledger accounts (and notations to the accounts), diaries or calendar entries.

Source:

Fringe benefits tax - record keeping exposure draft legislation | Treasury.gov.au

Travel diary

The current rules require an employer to collect travel diaries for any overseas travel and for domestic travel for a period of more than five nights where the travel is not wholly for business purposes.

The travel diary must include details of what the travel relates to, and dates and times of activities conducted during the trip.

Relocation transport

Where employees are required to relocate for work, employers may reimburse employees for travel using the cents per kilometre method and provided certain criteria are met, the reimbursement is exempt from FBT.

One of these criteria is the completion of an employee declaration that specifies who travelled in the car, the start and end locations of travel, make and model of the car, number of kilometres travelled and number of family members who travelled.

Some of the information required is unlikely to be collected outside of the current relocation transport declaration process. Accordingly, system changes may be required to take advantage of the legislative instrument. In the meantime, declaration templates (including for relocation transport) which meet the legislative requirements are available in ONESOURCE FBT.

4. Car Parking – Commercial Car Parking Facility

Employers impacted by the car parking changes effective 1 April 2022, should ensure they consider the various valuation methods available to calculate the number of car parking fringe benefits and the value of these benefits, to ensure the taxable value is minimised.

The ATO released TR 2021/2 in June 2021, which expanded the Commissioner’s view on the types of car parks that are considered commercial parking facilities.

As detailed in last year’s publication, this ruling set out that if a car park is operated by a car parking operator it is a commercial car parking facility, regardless of whether it is run on behalf of or within another building or business (e.g. Secure parking operating a hospital or shopping centre car park).

If a car park is not operated by a car parking operator it is a commercial parking facility if 2 of the 3 hallmark characteristics below are present:

- Has clear signage visible from the street advertising that paid parking is available

- Has mechanisms to control who can enter and/or exit the parking facility (for example boom gates or ticketing machines)

- Charges more than a nominal fee for paid parking

Of particular concern for many employers was that under the final ruling, from 1 April 2022, car parks such as those at shopping centres, hotels and hospitals charging penalty rates for all-day parking could no longer be ignored when determining whether a commercial parking station charged a fee over the daily car parking threshold ($9.72 for the year ending 31 March 2023).

However, this wasn’t the end of the matter, because in March 2022 the former Assistant Treasurer announced by media release that the Federal Government would be undertaking consultation with the intent of restoring the previously understood application of car parking fringe benefits. We are almost a year on from the announcement and with a new government in place, so it is increasingly unlikely that a consultation and subsequent legislation could be enacted in time for the 2022-23 FBT returns.

It is therefore important that employers holding off on reviewing the impact of the changes pending the outcome of the consultation, act now. Employers will need to consider each car parking location and how they will be valued for the year ending 31 March 2023.

There are three methods available to calculate the number of car parking fringe benefits that arise and three methods available to calculate the value of the car parking spaces. Employers are free to elect the method the minimises the taxable value. An overview of these methods is available within the ONESOURCE FBT Help guide.

5. Car Parking – Primary Place of Employment

Draft changes to TR 2021/2 were released by the ATO and address the concept of “primary place of employment”

Following the Full Federal Court decision in Commissioner of Taxation v Virgin Australia Regional Airlines Pty Ltd Limited [2021 FCAFC 209] in 2021, the ATO has updated TR 2021/2. These updates provide clarity on what the ATO considers the “primary place of employment” of an employee, which can be an important concept when determining whether car parking fringe benefits arise.

To determine an employee’s primary place of employment the draft ruling provides a two-step test for employers:

- Identification of the business premises which are the sole or primary place of employment of the employee. The draft ruling points to consideration of the employment conditions within the employment contract and/or industrial instrument (e.g. rostering, allowances and car parking entitlements) to assist with this process.

- If the first test cannot be satisfied, consideration of the place from which or at which the employee performs their duties though a qualitative and quantitative analysis of what the employees are doing and where.

Under this two-step test, the primary place of employment can be different to where the employee principally performs duties on a particular day.

Webinar available on demand

Hear about the biggest changes in FBT this year.

Hayley Lock

Partner

KPMG Employment Tax Advisory

Hayley Lock leads the Specialist Tax & Reward practice in Queensland and has over 15 years’ experience both in commerce and within professional services providing advice on a range of employment taxation matters. Hayley has worked with some of Australia’s largest employers and is also a current member of the ATO's FBT sub-committee. In her work with her clients she has advised on all employment tax related matters including PAYG withholding and reporting, payroll tax, Superannuation Guarantee, Workers Compensation Insurances and fringe benefits tax.

Stacey Biggar

Senior Manager

KPMG Employment Tax Advisory

Stacey Biggar is a director in KPMG’s Employment Tax team with 11 years’ experience assisting with employments tax matters including fringe benefits tax, superannuation guarantee, payroll tax, pay as you go withholding and workers compensation. Stacey has assisted a large number of clients with full FBT outsourcing projects and has extensive experience assisting a variety of clients with identifying and implementing process improvements and management of employment tax related issues including risk reviews, preparation and submission of voluntary disclosures with revenue authorities and advising on changes to legislation and practical implications.

Amesh De Silva

Proposition Manager

Thomson Reuters

Amesh leads the commercial strategy and product management of ONESOURCE Fringe Benefits Tax within Australia, along with providing go-to-market direction and focus for other ONESOURCE solutions.

Amesh has 7 years' experience as an accountant having previously worked at Commonwealth Bank and PwC in roles across finance, audit and advisory. Prior to Thomson Reuters, Amesh worked as the commercial lead of a software start-up that specialised in automated vehicle tax logbooks for FBT.

Amesh holds a Bachelor of Commerce with Finance & Economics from USYD and an MBA at AGSM.